Dear Friends and Colleagues, Once again, we start the October–December issue with a report on the monsoon. In all parts of India, we have had a normal monsoon and it is thought that agricultural outputs will likely be excellent for the season. Thus, many economists are predicting that there is a strong chance that India will return to GDP growth of 8% this year. Regrettably, the monsoon also resulted in major havoc in Kerala, which received unprecedented rain from 1 August to 19 August of 29.87 inches or 758.6 mm, resulting not only in total disruption and destruction of property but also a substantial loss of life. We at J.M. Baxi & Co. contributed to the relief efforts as best we could. Our heartfelt sympathies and support go to the people of Kerala. We hope to see them get back to normal as soon as possible.

Continuing the macroeconomic trend, one of the major areas of concern has been the sharp drop of the rupee against the US dollar. This is leading to an increase in fuel prices, which may have an impact on logistics and transportation costs. Whilst, at the moment, India seems relatively unscathed by the tariff wars that have begun in earnest between the US and China, the general global situation has contributed to the depreciation of the Indian rupee. Along with scrutinising the US–China trade tariff spat, the world will be watching closely the sanctions against Iran and more so the sanctions against Iran’s crude oil trade.

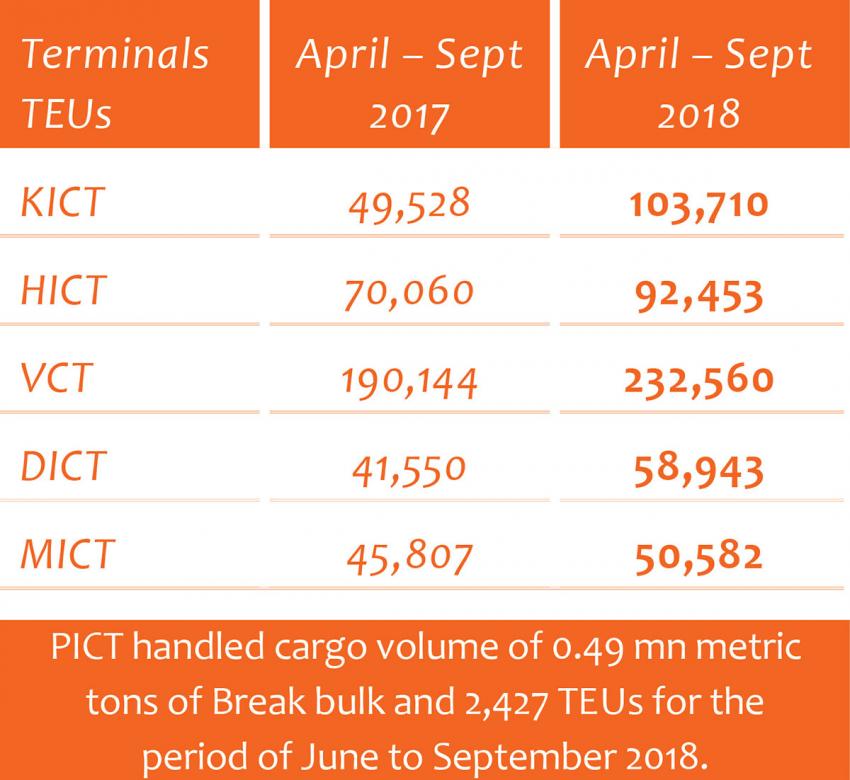

On a positive note, it is, therefore, very likely that we shall see intra-Asia trade continue to grow. The Indian economy has shrugged off its flatness of the last couple of years and growth in industrial production seems to be kicking firmly in. Agriculture is strong and with a successful monsoon, there should be no reason to see any decline. The ports and logistics sector confirms this assessment. Across all the ports as well as the inland terminals, we have seen that cargo volumes are holding steady. There has been a sustainable steady growth of trade across almost all commodities. In some areas, we are also noticing berthing delays, which is an indicator of good trade volumes.

On the container shipping line front, everyone is closely watching the US–China trade tariff spat with close interest. Any major disruption to China–USA trade lanes will impact the demand–supply equilibrium of ships and slots. Very large container ships (VLCCs) have not only been deployed, but more ships are being delivered for the Far East to Europe trade lane. Certainly, we are very much waiting and watching.

Bulk carriers seem to be holding their own, even though Vale continues to build and roll out its own Valemax tonnage, mainly for the ore trade to China from Brazil. The tanker markets remain sluggish and are causing increasing distress to shipowners.

In India, on the ports and coastal and river shipping front, we continue to see the Sagarmala project evolving. Linked to this, we are also observing the encouragement of the maritime cluster methodology. The Inland Waterways Authority of India is taking long strides in creating river terminals and dredging to enable the navigability of the river Ganges, i.e. National Waterway No 1.

On the logistics front, Boxco Logistics is involved in some interesting projects. With large-scale public transportation projects coming up in various parts of India, such as metros, and also the growth of the petroleum and petrochemical sector, we are looking forward to a busy and satisfying 2019.

The next edition, which will be January 2019, will include a report on the rollout of Portall PCS Ix for all the ports in India. With our ship agency and logistics units, we are mainly a service business. All services business are seeing incredible change. Walmart-Amazon, hotel chains- Airbnb, automobile companiesUber, Ola and Tesla. The change and disruption is for all to see. We are all seeing the great importance of artificial intelligence(AI), blockchain, digitalisation etc. Our colleagues in our group are working hard to keep us relevant, to keep us ahead, to keep us competitive. We will see incredible disruptions and we also see great opportunity.

This is the last quarter of the calendar year 2018. We entered 2018 knowing that it would be a tough year and we can proudly say that the year has been “not bad”.

The last quarter will see Durga Puja, Diwali, Christmas and of course the start of 2019. I take this opportunity to wish each of you and your families “Happy” festivities on these occasions. I welcome you to join us in 2019 with confidence and courage, as it seems it will be a great year ahead.

Till next time

Krishna B. Kotak

Chairman - J M BAXI

GROUP