There is no better alternative mode of transporting massive quantities of semi-finished and finished goods than container shipping across continents or within the region; even the launch of more freight train services or road network is unlikely to supplant transcontinental container shipping services.

Carriers were prone to financial pressures in 2016/2017, which proved to be a tumultuous period for the global shipping industry, with freight rates dipping to their lowest levels since 2009, there were announcements of Mergers, Acquisition, new alliances, closures and bankruptcies. Events like Brexit, new US administration policies, the blockade of Qatar which threaten to inject even more uncertainty into the future of global trade. Carriers that weather this storm will have an arduous task ahead of them, but to overpower the situation, carriers must build a business strategy with clearly defined focus on customer, route profitability, reduction in operating costs, fleet rationalization without being lost in the fast evolving technological advancement.

Ocean freight rates increased in 2017 due to consolidation, increase in bunker prices and regulated capacity growth, which also saw an increase in global container port throughput by 6.7 percent.

It has to be noted here that with the perpetual increase in operating cost, many firms are finding solace in Merger and Acquisition, whereas fleet regularization had also helped in raising industry concentration, empowering lines to better manage deployed capacity and preventing free-falling of freight.

Fortunately, the pace of M&A activity accelerated at the end of 2016 through 2017, carriers that have not been involved in a merger or acquisition are persistently rumored to be the next to do a deal and these consolidation will likely continue with smaller player falling prey, until there will only be 10 carriers in 2021.

We must also remark that the recent slew of M&A activities had helped increase the industry concentration, that will help improve the liners’ ability to better manage actual deployed capacity going forward, thereby reducing the probability of free-falling freight rates and gradually driving freight rate recovery.

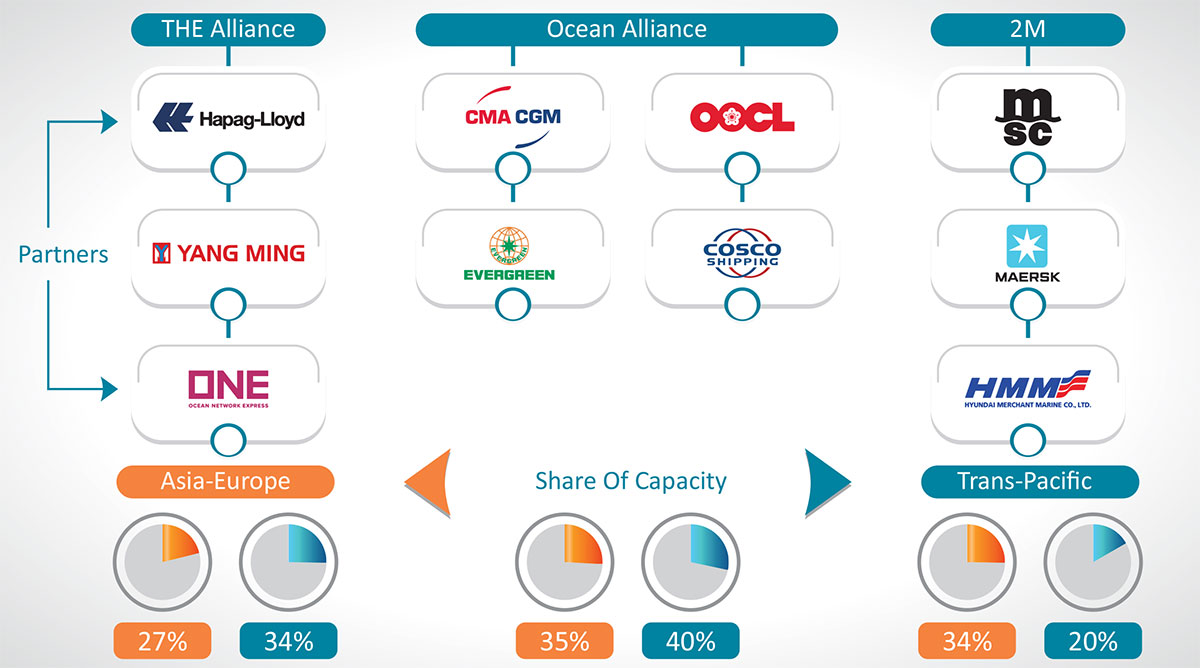

While, the top five liners traditionally controlled about 55% of capacity most of the capacity are now being controlled by the new alliances formed in 2017.

Intra-Far East and Intra-Europe trade lanes are dominated by 1,000-1,999 TEU size vessels and Europe-North America and Oceania related trade lanes are dominated by 4,000-5,099 TEUs vessels, due to which, 27% of the global idle vessels are in the range of 3,000 to 4,000 TEUs in size which are too small for the larger trade lanes and too big for the shorter sea trades, which is especially true after widening of the Panama Canal.

The current charter rates for 4,000 TEUs vessels are 36% lower than the rates for 1,700 TEUs vessels (source: Alphaliner). If these ships cannot find employment and are scrapped earlier than their useful lives, it would help restore the industry demand and supply balance much more quickly. The smaller displaced ships are likely to cascade into the other route regions where infrastructure is not a constraint.

Meanwhile in India . . .

The Union Cabinet having approved to replace the 'Major Port Trusts Act, 1963' by the 'Major Port Authorities Bill, 2016', will empower major ports to perform with greater efficiency by having full autonomy in decision making and by modernising the institutional structure of major ports, this should also help with meeting the set target capacity of 3,130 MMT by 2020, which would be driven by participation from the private sector.

With other new development under Sagarmala Programme, wherein, the government has envisioned a total of 189 projects for modernisation of ports involving an investment of Rs 1.42 trillion (US$ 22 billion by the year 2035) and the DPD scheme, which allows importers/consignees to take delivery of the containers directly from the port terminals which reduces the clearance time to 48 hours against an average of seven days at present, will all contribute to the improvement of infrastructure and process that will help in improving the container volume (International & Domestic) through the ports.

Trade statistics reveal that the Indian terminals have been growing at an average of 7% Year on Year, which is in line with the global throughput increase of 6%, which combined with the increase in average vessel size calling at Indian ports increasing to 5,500 Teus (excludes feeder and coastal services), with the JNPT average vessel call size reaching 6,000 Teus and Mundra averaging ships of 6500 TEUs. There is constant pressure on the terminals in India to focus infrastructure improvement and automation.

Increasing investments and cargo traffic point towards a healthy outlook for the Indian ports sector and the upscale of existing ship capacity to bigger ones, the continuous Mergers & Acquisitions of the lines, with the expected increase in freight rates, is expected to contribute to a better shipping environment globally and in India. However, what this year holds for the Global and Indian shipping trade is yet to be seen, as the famous saying goes "THE TRUTH IS OUT THERE".