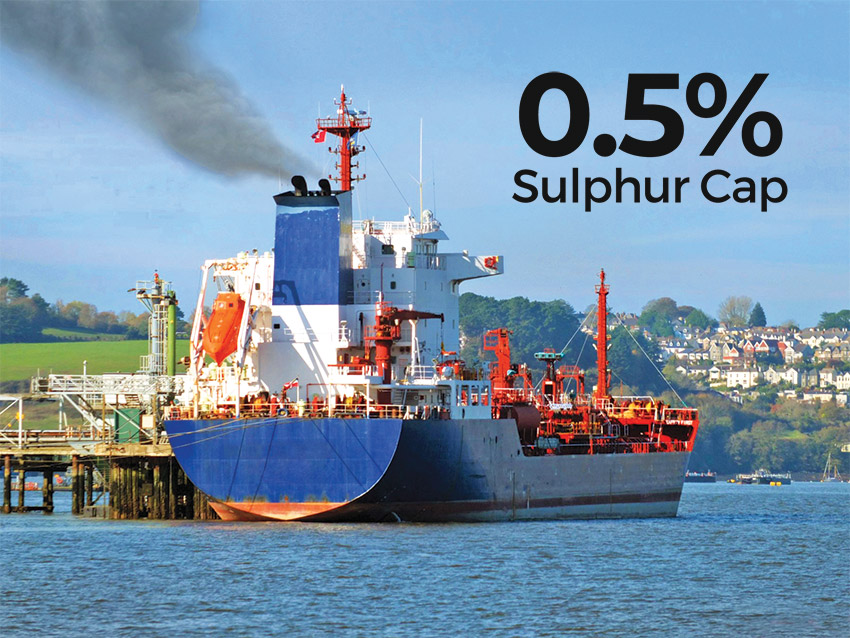

International Maritime Organisation widely known as ‘IMO 2020’ is the popular topic in the maritime fraternity as the industry braces to implement the new Sulphur Cap Guidelines on Buner Fuel coming into effect from 1st January 2020. This resolution adopted at the 70th meeting of the IMO’s Maritime Environment Protection Committee held in October 2016, limits the Sulphur content in marine fuels to 0.5 per cent from 3.5 per cent that is presently allowed.

The Global Fuel Sulphur Cap is part of the IMO’s response to controlling harmful emissions from ships. This resolution was first adopted by IMO in the year 1995, whereby effective from January 2005, the Sulphur content in bunker fuel was limited to 4.5 per cent. This limit was further lowered to 3.5 per cent in 2012 and is the one prevailing limit now. The IMO had also designated few geographic areas as Sulphur Emission Control Areas (ECA) where Ships have to burn bunker fuel with a sulphur content of no more than 0.1 per cent. This has been in effect since 1 January 2015 and includes geographies like Baltic Sea, the North Sea, parts of the North American and the US Caribbean Sea.

In international shipping, majority of the Merchant Ships use heavy fuel oil (HFO) which is the traditional source of energy to power ships and accounts for over 70 per cent of all Bunker fuels. The rest is Low-Sulphur Marine Gas Oil (MGO) with below 0.5 per cent of Sulphur content and the Ultra Low Sulphur Fuel Oil (ULSFO) with below 0.1 per cent of sulphur content used in ECAs. The new resolution is, therefore, going to impact a huge part of the maritime industry and has sent the entire Shipping industry as well the Bunker Oil Supplying industry into a quandary as to how would things evolve post 1st January 2020. There have been series of papers written as well as discussions happening at various forums as operators are running against the clock to meet the deadline.

For compliance,

- Shipowners have the following three options

- Use Low Sulphur Fuel (LSF) or Marine Gas Oil (MGO) containing less than 0.5 per cent of Sulphur content.

- Continue to use the Heavy Fuel Oil and install Scrubbers in the ships which would capture the Sulphur content from exhaust fumes

- Use LNG as bunkers

None of the above is an easy solution which can be adopted at the switch of a button and hence, the confusion and the distress in the industry. The problem is compounded further by the fact that Shipping industry has been going through a phase of depressed freight rates in the last few years and Shipping companies are not generating large cash surplus to increase their capital or operational expenses at this point of time.

- The way ahead with either of the options

-

A. Heavy Fuel consumption by ships was about 3.5 million barrels per day in 2018 (about 175 million tonnes for the full year). In case, the entire world fleet of merchant ships switch over to Low Sulphur Fuel, the world refining capacity is not geared to produce so much of clean fuel from 1st January. Refineries worldwide have been looking at high Sulphur fuel sales as a way of disposing of their Sulphur residues in the distillation chain. With a stoppage of such sales from January 2020, Refineries will have to find a way to dispose off their Sulphur residues. Hence, this is going to change the entire Bunker oil Refining and Marketing chain. Although, major Oil Companies have confirmed that they would be able to supply the Low Sulphur Fuel from end of 2019 and Shipping Companies need not worry about supplies, industry experts still doubt on seamless availability of this fuel in all geographies.

Apart from the supply worries, cost of LSF is the biggest concern Ship operators have. Presently MDO is far more expensive than HFO and if Ships are going to use MDO or LSF for their ocean voyages, Operational costs for Shipping Companies are going to sky rocket. As is well known, Bunker costs are the single largest cost head during vessel operations and the switch over to LSF or MDO is going to increase costs for Ship operations. How much of this increase can be passed over to the Trade in terms of increase in freight is yet to be seen, but the fact remains Logistics costs of Goods are set to increase post January 2020.

-

B. The second option for Shipowners to install Scrubbers on their vessels which would capture the Sulphur emissions from the exhaust gases limiting its content to prescribed limit, whilst continuing to burn Heavy oil as Bunkers. This technology works by spraying alkaline water into a vessel’s exhaust which removes Sulphur and other unwanted Chemicals. This innovative concept is easier to speak than to be put in motion. Scrubbers can be of two types - Closed loop and Open loop. A Closed loop Scrubber would capture all the excess Sulphur from exhausts and then this Sulphur would be disposed off at Port receiving facilities during the vessel’s call at Ports. Whereas an Open loop Scrubber would capture the excess Sulphur from the exhaust gases and would then dispose-off the captured Sulphur in smaller quantities during its voyage in high seas, which is permissible under international laws. There have been many concerns on use of Open loop Scrubbers as its going to pollute the Ocean where the Sulphur is discharged. Many countries have announced that they would not be accepting Vessels to operate Open loop Scrubber within their territorial limits. Hence a vessel fitted with Open loop Scrubber would have to switch over to LSF or MDO during calls at these restrictive ports.

Whilst the above are operational difficulties in usage of Scrubbers, the first problem is installation of Scrubbers on vessels, whether Closed or Open loop. Fitting a Scrubber in a new vessel under construction is simple as the Engine room layout can be designed that way. However, for existing vessels, finding out space within the engine room for fitting a Scrubber has been a major challenge. Next, even if the Engine layout within a vessel can be modified, finding adequate number of Repair Yards which can carry such modification for the huge number of world fleet has been a major challenge. Fitting a Scrubber on an existing vessel can take anywhere between one month to four months at a shipyard/repair yard. That means an exiting drydock can refurbish a maximum of 12 vessels in a year and if the entire world merchant fleet were to install Scrubbers, it would take years to complete such mammoth project.

Finally, the most difficult issue on fitting Scrubbers is the financial viability. A ballpark figure on fitting a Scrubber is anywhere between USD 2 million to 8 million, depending upon the size of vessel and location of yard. In the prevailing depressed freight market scenario, such a huge investment may not be justifiable and shipowners are averse to investing this additional amount on their vessels looking at the cost–benefit analysis. It is difficult to predict if the freight earnings would increase post January 2020, to compensate for this additional capital cost. In case the vessel is old with a short balance life, amortising this additional cost over the balance life can be a challenge. In case the vessel is operating on a trade segment where the voyages are short and port stay is longer, it does not make sense to invest in installation of Scrubbers. Hence there are many dynamics affecting this option and not many shipowners are therefore going for this option for their existing fleet.

-

C. The Third option shipowners have is to switch to LNG as bunker fuel. Ships can switch over to LNG as bunker fuel with minimal change to their engines and LNG is the cleanest fuel any vessel can use. However, this again is not a viable solution as there is no LNG bunkering infrastructure available worldwide today. LNG bunkering infrastructure is at an infant stage today as most LNG-powered ships are mainly coastal vessels limited to European waters. There continues to be interest in many other countries in developing LNG bunkering infrastructure, but such development cannot come up in the short term. There is a need to set up entire Supply Chain logistics, increase Storage Space, set up facilities at Ports, Pipelines, etc. Building up such LNG supply infrastructure is far more complex and expensive than building normal Bunker fuel supply infrastructure, hence this option may not be a viable option for majority of the world fleet.

Time is running out for Shipping industry to opt from one of the above solutions and due to the lack of clarity on how the freight markets would react to this new regulation, majority of the players are likely to adopt burning Low Sulphur Fuel rather than going for expensive retrofitting of Scrubbers on existing fleet. As of date, very few shipping companies have gone in for Scrubbers on their existing fleet. Going ahead the new buildings may be fitted with Scrubbers and the existing fleet continue with same Engine set ups. Thus, there would be a mix of HFO and LSF bunker requirements of the shipping industry. Whether this would mean a differential freight rates for vessels burning HFO vis-à-vis vessels burning LSF, is a question difficult to answer at this point of time.